CGST, SGST, IGST: what the three GST taxes on your bill actually mean

A shopkeeper's plain-English guide to CGST, SGST and IGST — why a bill splits the tax into two within your state, charges one IGST line across states, and why the customer pays the same either way.

Look at any GST bill and you’ll see the tax written one of two ways. A sale inside your own state shows two lines — CGST and SGST — each carrying half the tax. A sale to another state shows a single line: IGST, carrying the whole thing. Same product, same rate, different labels. The first time you notice it, the natural worry is that selling across a state border costs more. It doesn’t, and this guide is about why.

Same sale, same ₹1,800 tax. Within your state it splits into CGST and SGST; across states it’s a single IGST line.

One rule decides which you charge

Everything comes down to whether the sale stays inside your state or crosses out of it.

- Same state (you and the buyer are in the same state): the tax splits into CGST and SGST, each at half the rate. CGST goes to the central government, SGST to your state government.

- Different states (the goods go to a buyer in another state): you charge IGST instead, at the full rate, as one line. The central government collects it and passes the state’s share to the state where the goods end up.

That’s it. CGST plus SGST always equals IGST, because IGST is just the two of them combined into a single charge.

A bill makes it obvious

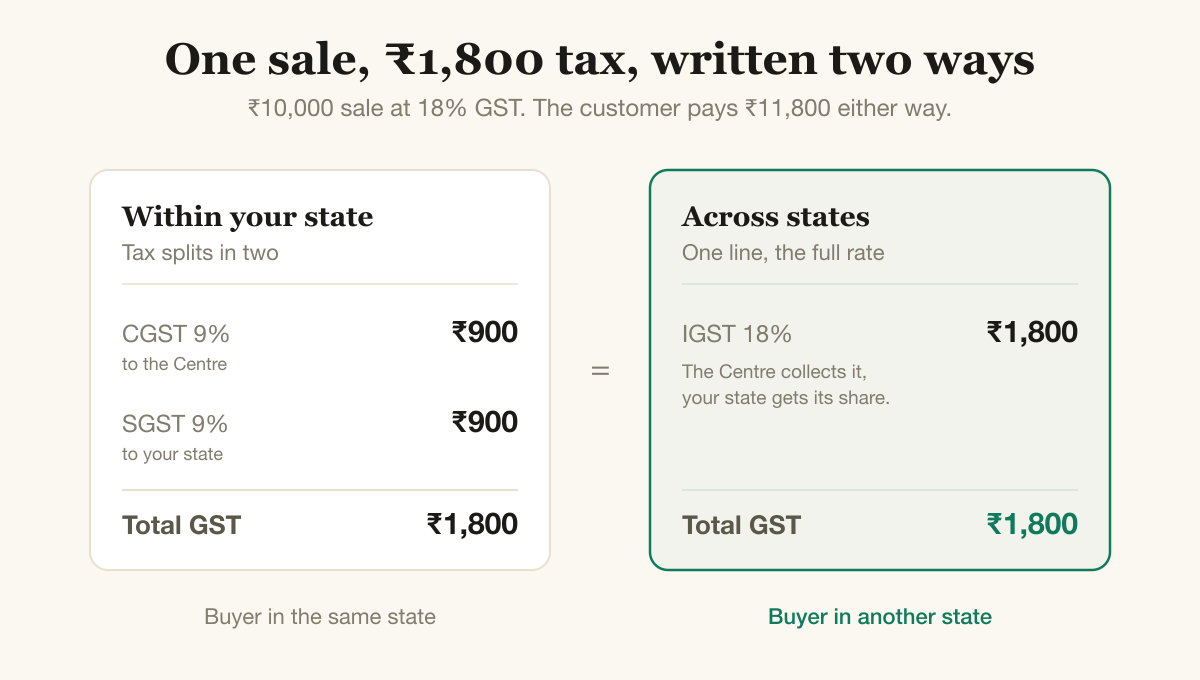

Take a ₹10,000 sale at 18% GST.

Sold to a customer in your own state, the bill reads:

| Tax | Rate | Amount |

|---|---|---|

| CGST | 9% | ₹900 |

| SGST | 9% | ₹900 |

| Total GST | 18% | ₹1,800 |

Sold to a customer in another state, the same ₹10,000 reads:

| Tax | Rate | Amount |

|---|---|---|

| IGST | 18% | ₹1,800 |

Both bills come to ₹11,800. The tax is ₹1,800 either way. What changes is the label on the bill and which government the money flows to — never the amount your customer pays. So if a buyer in another state ever asks why their bill says IGST and a local buyer’s says CGST and SGST, the honest answer is: it’s the same tax, written for a sale that left the state.

What counts as “another state”?

The rule that decides it is the place where the goods are supplied, not the address a buyer happens to write down. For a normal shop, that lands in two simple cases:

- A customer walks in and buys something over the counter. The goods change hands in your state, so it’s a same-state sale: CGST and SGST.

- You ship or courier goods to a buyer in another state. The goods end their journey there, so it’s an inter-state sale: IGST.

Most of the time the buyer’s state and the delivery state are the same, so you rarely have to think harder than “did this leave my state or not.”

Where UTGST fits

A handful of Union Territories don’t have their own legislature — Chandigarh, Lakshadweep, the Andaman and Nicobar Islands, Ladakh, and Dadra and Nagar Haveli and Daman and Diu. A sale inside one of those replaces SGST with UTGST, the Union Territory version. It works exactly like SGST, the same half-the-rate split alongside CGST. Union Territories that do have a legislature, like Delhi and Puducherry, use regular SGST. For billing, UTGST behaves identically to SGST; only the name on the line changes.

Why the tax is split at all

The split isn’t there to make your life harder. It exists because two governments, the Centre and your state, each levy GST on the same sale and each keep their half. Splitting it into CGST and SGST is how the bill shows whose money is whose.

It also ties into input tax credit, which is the part that keeps GST from taxing the same goods twice. When you buy stock for your shop, you pay GST on that purchase. When you sell it, you collect GST from your customer. You hand the government only the difference — the tax on the value you added, not on the full sale price. One practical wrinkle worth knowing: credit from the CGST you paid can offset CGST you owe, and SGST credit offsets SGST, but the two don’t cross over directly. For a shop that buys and sells within one state, this stays in the background; your billing simply shows CGST and SGST, and the credit lines up on its own.

Did the 2025 GST reform change any of this?

The GST 2.0 reform that took effect on 22 September 2025 rewrote the rate slabs — it merged the old four rates down to mainly 5% and 18%, with a 40% rate for luxury and sin goods. It left the CGST, SGST and IGST structure completely untouched. Same state still means CGST plus SGST; another state still means IGST. The reform changed how much tax, not how it’s split.

Getting it right on every bill

The one mistake that’s easy to make by hand is charging CGST and SGST on a sale that should be IGST, or the reverse — usually by going off the buyer’s billing address instead of where the goods actually go. Get it wrong and your GST return won’t reconcile.

Kwibo works it out for you. You pick the buyer’s state, and it reads the state codes to decide: CGST and SGST within your state, IGST across states, split correctly every time. No login, no account — open it, make the bill, and the tax lines come out right. And because the customer can read the bill in their own language, an IGST line doesn’t have to be a line they take on faith.